Did you know that according to the National Association of Dental Plans (NADP), over 75% of Americans have some form of dental coverage? While this number is encouraging, understanding the actual cost of that coverage for a family can be a complex puzzle. Dental insurance isn’t a one-size-fits-all product, and the price you pay can vary significantly based on numerous factors. This guide aims to demystify the expenses associated with dental insurance for families, helping you make informed decisions to protect your loved ones’ smiles and your budget.

The Foundation of Dental Insurance Costs: What Influences the Price?

Before diving into specific figures, it’s crucial to understand the building blocks that determine how much you’ll pay for family dental insurance. These factors are interconnected and collectively shape the premiums and out-of-pocket expenses you can expect.

1. Type of Dental Insurance Plan

The most significant driver of cost is the type of dental insurance plan you choose. The two primary categories are:

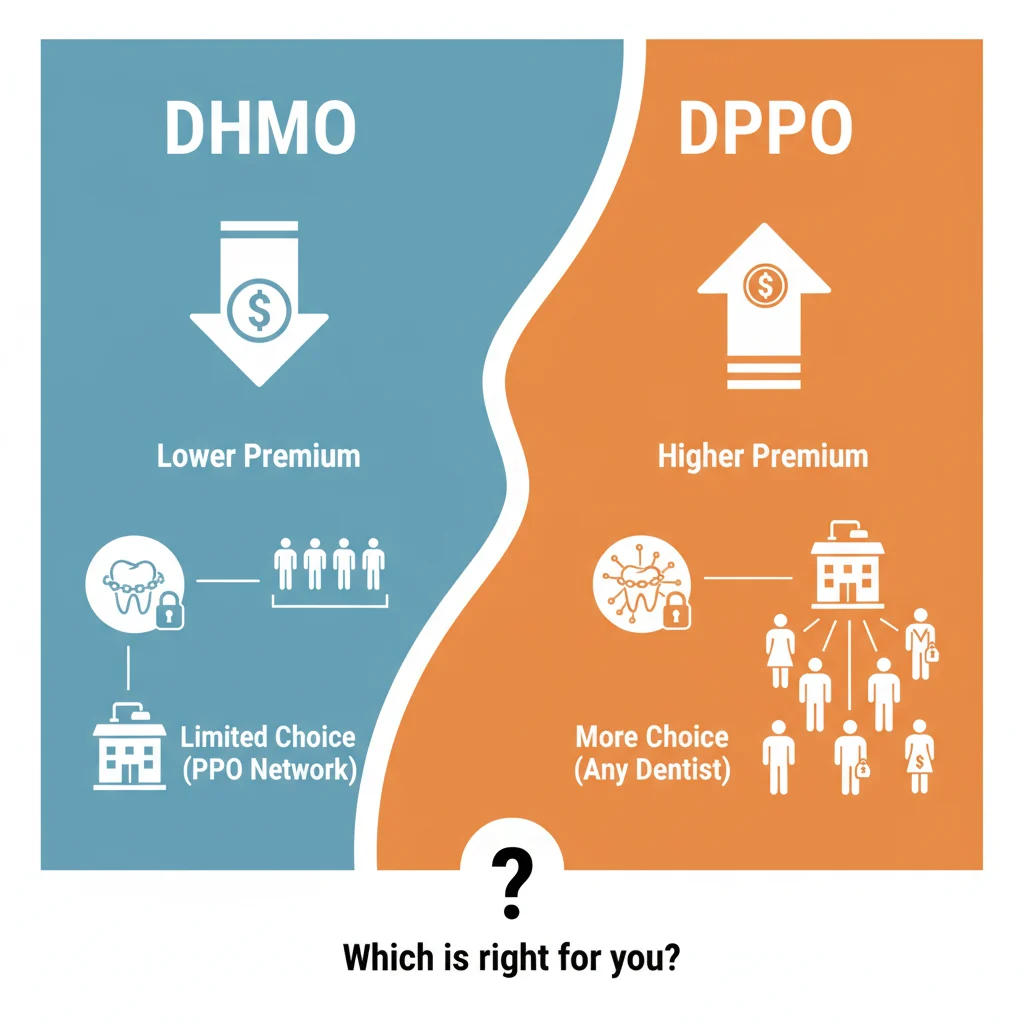

- Dental Health Maintenance Organization (DHMO): These plans typically have lower premiums and often require you to select a primary dentist and get referrals to see specialists. While generally more affordable, they can offer less flexibility in choosing providers.

- Dental Preferred Provider Organization (DPPO): DPPO plans usually have higher premiums than DHMOs but offer more freedom to choose dentists within a network. You generally don’t need referrals to see specialists, and you may have coverage for out-of-network providers, albeit at a higher cost.

“The choice between a DHMO and a DPPO often comes down to a trade-off between cost and flexibility,” explains Dr. Emily Carter, a practicing dentist with over 15 years of experience. “Families prioritizing lower monthly payments might lean towards a DHMO, while those who value provider choice and easier access to specialists might find a DPPO more suitable, despite the higher premium.”

2. Geographic Location

Where you live plays a surprisingly significant role in dental insurance costs. Dental care costs, including the price of insurance, tend to be higher in metropolitan areas and regions with a higher cost of living. This is often due to higher overhead costs for dental practices, such as rent and staffing, which are then reflected in insurance premiums.

3. Age of Family Members

While most dental insurance plans don’t drastically increase premiums based solely on age for adults, certain plans might have slight variations. However, the need for dental care can increase with age, impacting out-of-pocket expenses. Children, for instance, may require more frequent check-ups and potentially orthodontic treatment, which can influence the overall financial picture.

4. Coverage Level and Benefits

The more comprehensive the coverage, the higher the premium will likely be. Dental insurance plans are structured with different levels of benefits, often categorized as:

- Preventive Care: Usually covered at 100% (e.g., cleanings, exams, X-rays).

- Basic Restorative Care: Often covered at 70-80% (e.g., fillings, simple extractions).

- Major Restorative Care: Typically covered at 50-60% (e.g., crowns, bridges, dentures, root canals).

- Orthodontics: Coverage for braces and other alignment treatments can vary widely, often with a separate annual maximum or lifetime maximum.

Plans that offer higher reimbursement percentages for basic and major procedures, or those with more generous annual maximums, will naturally cost more.

5. Annual Maximums

Most dental insurance plans have an annual maximum benefit, which is the most the insurance company will pay for dental care in a given year. This limit can range from $1,000 to $2,000 or more. Plans with higher annual maximums often come with higher premiums, as they offer greater financial protection for extensive dental work.

6. Deductibles

A deductible is the amount you pay out-of-pocket before your insurance plan starts covering costs. Some plans have no deductible for preventive services, while others may have deductibles for basic and major procedures. Plans with lower deductibles generally have higher premiums, and vice-versa.

7. Waiting Periods

Many dental insurance plans have waiting periods before certain benefits become active. For example, there might be a 6-month waiting period for basic restorative services and a 12-month waiting period for major restorative services. While not a direct cost, waiting periods can influence your decision-making and the immediate out-of-pocket expenses you might incur.

8. Network vs. Out-of-Network Coverage

As mentioned with DPPOs, plans often have networks of dentists. Using an in-network dentist usually results in lower costs because the insurance company has negotiated rates with these providers. Going out-of-network typically means higher out-of-pocket expenses.

9. Rider Benefits

Some plans offer optional rider benefits, such as enhanced coverage for orthodontics or cosmetic procedures. Adding these riders will increase the overall cost of the plan.

Average Costs of Family Dental Insurance

Pinpointing an exact average cost for family dental insurance is challenging due to the myriad of variables. However, we can provide estimates based on common plan types and family structures.

Individual vs. Family Plans

- Individual Dental Plans: These are designed for a single person and will be the least expensive option.

- Family Dental Plans: These plans cover multiple individuals, typically two adults and their dependent children. The cost of a family plan is almost always more than twice the cost of an individual plan, but often less than the combined cost of multiple individual plans.

Estimated Monthly Premiums

Based on data and industry averages, here are some estimated monthly premium ranges for family dental insurance:

- Low-Cost Plans (e.g., basic DHMOs): $30 – $60 per month

- Mid-Tier Plans (e.g., standard DPPOs with good coverage): $60 – $120 per month

- Premium Plans (e.g., comprehensive DPPOs with high annual maximums and low deductibles): $120 – $200+ per month

Important Note: These are estimates. Actual costs can be higher or lower depending on the specific factors mentioned above and the insurance provider.

Beyond Premiums: Understanding Out-of-Pocket Costs

While monthly premiums are a significant part of the cost, they are not the only financial consideration. Your out-of-pocket expenses will also play a crucial role in the overall cost of dental care for your family. These include:

Deductibles

As previously discussed, you’ll pay your deductible before your insurance starts contributing to the cost of certain procedures. Family plans may have individual deductibles (per person) or a family deductible (which applies once a certain amount is met by the family as a whole).

Copayments (Copays)

A copayment is a fixed amount you pay for a covered dental service after you’ve met your deductible. For example, you might have a $20 copay for a routine check-up or a $50 copay for a filling. Copays are more common with DHMO plans.

Coinsurance

Coinsurance is your share of the costs of a covered dental service, calculated as a percentage of the allowed amount for the service. For instance, if your plan covers 80% of a filling, you would be responsible for the remaining 20% (your coinsurance). This applies after you’ve met your deductible.

Annual Maximums

Once your plan reaches its annual maximum benefit, you will be responsible for 100% of the cost of any further dental treatments for the rest of that year. This is why choosing a plan with an appropriate annual maximum is vital, especially for families who anticipate needing more extensive procedures.

Strategies for Managing Family Dental Insurance Costs

Navigating the costs of dental insurance can feel overwhelming, but several strategies can help you manage expenses effectively:

1. Compare Plans Thoroughly

Don’t settle for the first plan you see. Utilize online comparison tools and work with insurance brokers to explore various options. Pay close attention to:

- Premiums: The monthly cost.

- Deductibles: How much you pay upfront.

- Copays and Coinsurance: Your share of the costs for different services.

- Annual Maximums: The limit of coverage per year.

- Provider Network: The dentists available to you.

- Covered Services: What procedures are included and at what percentage.

2. Leverage Preventive Care

Most dental insurance plans cover preventive services like cleanings and exams at 100%. By attending these regular appointments, you can catch potential problems early when they are less expensive and easier to treat. This proactive approach can save your family significant money in the long run by preventing the need for more costly procedures down the line.

3. Understand Your Benefits “Use It or Lose It”

Dental insurance benefits typically reset annually. If you don’t use your annual maximum, you generally won’t roll over unused benefits to the next year. If you have been putting off a dental procedure and have benefits available, consider scheduling it before the end of the year.

4. Inquire About Dental Discount Plans

While not true insurance, dental discount plans can offer savings on dental services. You pay a monthly or annual fee, and in return, you receive discounts on a wide range of dental procedures performed by participating dentists. These can be a good option for those who don’t qualify for traditional insurance or find premiums too high. However, it’s crucial to understand that these are discounts, not insurance coverage, meaning you pay the discounted price directly to the dentist.

5. Consider Employer-Sponsored Plans

If you or your spouse have access to dental insurance through an employer, this is often the most cost-effective option. Employers frequently subsidize a portion of the premium, significantly reducing the cost to the employee. These plans are often PPO or DHMO and can provide excellent coverage.

6. Explore Government Programs and Affordable Care Act (ACA) Options

While the ACA primarily focuses on medical insurance, some states offer dental coverage as part of their children’s health insurance programs. Additionally, some marketplace plans may include pediatric dental coverage as an essential health benefit. For adults, standalone dental plans can be purchased through the ACA marketplace.

7. Ask About Payment Plans and Financing

If you need extensive dental work and your insurance doesn’t cover the full cost, ask your dentist about payment plans or financing options. Many dental offices partner with third-party financing companies to help patients manage the cost of treatment.

8. Utilize Your Dental Insurance Guide

Resources like Dental Coverage Guide can be invaluable. They provide information on understanding dental insurance terminology, comparing plans, and navigating the complexities of dental benefits. Using such guides can empower you to make more informed decisions.

Common Dental Procedures and Their Insurance Coverage

Understanding how insurance typically covers common dental procedures can help you budget and anticipate costs:

Routine Check-ups and Cleanings

- Coverage: Usually covered at 100% by most plans.

- Frequency: Typically recommended every six months.

- Cost Impact: Minimal out-of-pocket for insured individuals.

X-rays

- Coverage: Often included with preventive care, covered at 100%.

- Frequency: Varies based on dental needs, but often done annually or biannually.

Fillings

- Coverage: Falls under basic restorative care. Typically covered at 70-80% after the deductible.

- Cost Impact: You’ll pay the deductible plus your coinsurance percentage.

Root Canals

- Coverage: Considered a major restorative procedure. Typically covered at 50-60% after the deductible.

- Cost Impact: Can be significant, as root canals are complex and expensive.

Crowns

- Coverage: Also a major restorative procedure, often covered at 50-60% after the deductible.

- Cost Impact: Similar to root canals, crowns can be a substantial out-of-pocket expense.

Extractions (Simple and Surgical)

- Coverage: Simple extractions often fall under basic restorative care (70-80%), while surgical extractions may be considered major (50-60%).

- Cost Impact: Varies based on complexity and whether it’s basic or major.

Dentures and Bridges

- Coverage: Major restorative procedures, typically covered at 50-60% after the deductible.

- Cost Impact: These are expensive prosthetic devices, so coinsurance can add up.

Orthodontics (Braces)

Coverage: Varies greatly*. Some plans offer a percentage of coverage up to a lifetime maximum (e.g., 50% up to $1,500). Others may not cover adult orthodontics at all. Pediatric orthodontic coverage is more common.

- Cost Impact: Can be a significant expense, even with insurance, due to high treatment costs.

When Dental Insurance Might Not Be Enough

It’s important to acknowledge that even with dental insurance, significant out-of-pocket costs can arise, especially for families facing major dental work or those with lower annual maximums. According to a survey by the American Dental Association (ADA), the average cost of a crown can range from $700 to $2,000 or more, and orthodontic treatment can cost between $3,000 and $7,000. Even with 50% coverage after a deductible, these procedures can still leave families with hundreds or thousands of dollars in expenses.

This is where careful plan selection, understanding your benefits, and exploring additional financial strategies become paramount. For instance, if your family has a history of dental issues or anticipates needing extensive work like orthodontics, opting for a plan with a higher annual maximum and better coverage for major procedures, even with a higher premium, might be more cost-effective in the long run.

Conclusion: Investing in Your Family’s Oral Health

The cost of dental insurance for a family is not a fixed figure but rather a dynamic equation influenced by plan type, coverage levels, geographic location, and individual needs. While premiums are a primary concern, understanding deductibles, copayments, coinsurance, and annual maximums is equally vital for a complete financial picture.

By diligently comparing plans, prioritizing preventive care, and exploring all available resources, families can find dental insurance that balances affordability with comprehensive protection. Investing in dental insurance is not just about managing immediate costs; it’s about safeguarding your family’s long-term oral health, preventing painful and expensive emergencies, and ensuring bright smiles for years to come. Resources like Dental Coverage Guide are excellent starting points for demystifying this essential aspect of family healthcare.

—

Frequently Asked Questions About Family Dental Insurance Costs

The average monthly cost for family dental insurance can range widely, typically from $30 to $200 or more. This significant variation depends on the type of plan (DHMO vs. DPPO), the level of coverage, the number of family members, the geographic location, and the specific benefits offered by the insurance provider. Low-cost plans might be on the lower end, while comprehensive plans with high annual maximums will be at the higher end.

Coverage for orthodontics, particularly for children, varies significantly among dental insurance plans. Many plans offer some level of coverage, often a percentage (e.g., 50%) up to a specific lifetime maximum benefit (e.g., $1,000 or $1,500). Some plans may have waiting periods or specific requirements for orthodontic coverage. It’s crucial to review the plan details carefully to understand the extent of orthodontic benefits, including any age limitations or required waiting periods.

Family dental insurance plans can have deductibles structured in two main ways: an individual deductible (where each family member has their own deductible to meet) or a family deductible (where a certain combined amount must be met by the family as a whole before benefits kick in for certain services). Often, preventive services are covered at 100% and may not require a deductible. It’s important to check the plan’s specifics to understand how deductibles apply to each family member and for different types of services.

Generally, it is more cost-effective to purchase a single family dental plan than to buy individual plans for each member. Family plans are designed to cover multiple individuals under one policy, and while the premium is higher than an individual plan, it’s usually less than the combined cost of multiple individual policies. Additionally, family plans often simplify administration and ensure consistent coverage across all family members.

DHMO (Dental Health Maintenance Organization) plans typically have lower monthly premiums compared to DPPO (Dental Preferred Provider Organization) plans. This lower cost is often because DHMOs offer less flexibility in provider choice and usually require you to select a primary dentist and get referrals for specialists. DPPO plans, while generally more expensive in terms of premiums, offer greater flexibility in choosing dentists (both in and out-of-network) and usually do not require referrals. The out-of-pocket costs for specific procedures can also differ; DHMOs may have lower copays for in-network services, while DPPOs might have higher coinsurance percentages for out-of-network care.

To find affordable dental insurance, you should:

– Compare plans: Use online tools and work with brokers to see various options.

– Check employer benefits: Employer-sponsored plans are often the most affordable due to subsidies.

– Look at ACA marketplace plans: These may include pediatric dental coverage.

– Consider dental discount plans: These aren’t insurance but offer savings.

– Prioritize preventive care: Regular check-ups can prevent costlier issues later.

– Understand your needs: Choose a plan that covers the services your family is most likely to need without overpaying for unnecessary benefits.

—

Sources:

- National Association of Dental Plans (NADP). (n.d.). Dental Benefits: A Consumer Guide. Retrieved from https://www.nadp.org/ (Note: Specific publication details may vary, but NADP is the authoritative source for dental benefits statistics).

- American Dental Association (ADA). (n.d.). Health Policy Institute. Retrieved from https://www.ada.org/en/advocacy/health-policy-institute (Note: The ADA provides extensive data on dental costs and practice economics).

- Centers for Medicare & Medicaid Services (CMS). (n.d.). Health Insurance Marketplace. Retrieved from https://www.healthcare.gov/ (Note: CMS oversees the ACA marketplace, which includes information on essential health benefits like pediatric dental care).

Alex Carter

Alex Carter is an editor at Dental Coverage Guide, where he reviews dental insurance and dental coverage content for clarity, readability, and practical value. He focuses on helping U.S. readers better understand dental plan costs, coverage limits, provider networks, waiting periods, and plan options.